1. Understanding Medicare Enrollment

Medicare serves as the United States’ federal health insurance program primarily for individuals aged 65 or older. It also extends coverage to certain younger individuals with disabilities, End-Stage Renal Disease (ESRD), or Amyotrophic Lateral Sclerosis (ALS).As individuals approach the age of 65, understanding the intricacies of Medicare enrollment becomes paramount. Timely and informed decisions are crucial to secure necessary health coverage, avoid potential lifelong financial penalties, and prevent gaps in insurance that could lead to significant out-of-pocket expenses.

This report provides a comprehensive guide for individuals nearing age 65, outlining Medicare eligibility requirements, the enrollment process facilitated by the Social Security Administration (SSA), critical enrollment periods, and detailed explanations of Medicare Part B (Medical Insurance) and Medicare Part D (Prescription Drug Coverage). The objective is to equip individuals with the knowledge needed to navigate the system effectively and make crucial choices about their healthcare coverage. This report is accurate to the best of my knowledge, but things are always changing so accuracy is not guaranteed.

Overview of Medicare Parts

Medicare is structured into different parts, each covering specific types of healthcare services. Understanding these parts is fundamental to making appropriate enrollment decisions.

- Medicare Part A (Hospital Insurance): Primarily covers inpatient hospital stays, care in a skilled nursing facility (following a qualifying hospital stay), hospice care, and some home health care services.

- Medicare Part B (Medical Insurance): Covers medically necessary services from doctors and other healthcare providers, outpatient care, preventive services, durable medical equipment (DME), and some home health care.

- Medicare Part C (Medicare Advantage): An alternative way to receive Medicare benefits (Parts A and B, and usually Part D) through private insurance plans approved by Medicare. These plans often include additional benefits like vision, hearing, and dental coverage but typically have network restrictions. Enrollment in Part C is optional and requires prior enrollment in Parts A and B.

- Medicare Part D (Prescription Drug Coverage): Helps cover the cost of outpatient prescription drugs. This coverage is offered through private insurance plans (either standalone Prescription Drug Plans (PDPs) or integrated into Medicare Advantage plans (MA-PDs)).Enrollment is optional but recommended to avoid penalties if coverage is needed later.

While the Social Security Administration manages enrollment into Original Medicare (Parts A and B), individuals must proactively choose and enroll in Part C or Part D plans through private insurers, typically via the official Medicare website (Medicare.gov), during specific enrollment periods.Decisions about Parts C and D are often made concurrently with or shortly after enrolling in Parts A and B, highlighting the interconnected nature of Medicare choices.

2. Are You Eligible for Medicare?

Eligibility for Medicare is primarily based on age or specific health conditions, along with citizenship and residency requirements.

General Eligibility Criteria

The most common path to Medicare eligibility is turning 65 years old.To qualify based on age, an individual must also be a U.S. citizen or a permanent resident who has lawfully resided in the United States for at least five continuous years prior to applying.

Medicare eligibility is also extended to individuals under 65 under specific circumstances:

- Receiving Social Security Disability Insurance (SSDI) or Railroad Retirement Board (RRB) disability benefits for 24 months.

- Having End-Stage Renal Disease (ESRD), which is permanent kidney failure requiring dialysis or a transplant.

- Having Amyotrophic Lateral Sclerosis (ALS), also known as Lou Gehrig’s disease.

It is important to note that receiving Supplemental Security Income (SSI) alone does not automatically qualify an individual for Medicare; they must meet one of the other primary eligibility criteria.

Medicare Part A (Hospital Insurance) Eligibility

Eligibility for Part A, particularly whether it requires a monthly premium, is closely tied to an individual’s (or their spouse’s) work history and payment of Medicare taxes.

- Premium-Free Part A: The vast majority of individuals qualify for Part A without paying a monthly premium. This is typically achieved if the individual or their spouse has worked for at least 40 calendar quarters (equivalent to 10 years) in any job where they paid Medicare taxes in the U.S.. Eligibility for Railroad Retirement benefits or specific periods of federal or state/local government employment can also qualify an individual for premium-free Part A .Verifying one’s work history or a spouse’s work history with the Social Security Administration (SSA) is advisable if there is uncertainty about meeting the 40-quarter requirement.

- Premium Part A: Individuals who do not meet the requirements for premium-free Part A may still be able to enroll by paying a monthly premium, provided they are eligible for Part B and choose to enroll in it. The premium amount depends on the number of quarters worked:

-

- For individuals with 30-39 quarters of Medicare-covered employment, the 2025 Part A premium is $285 per month.

- For individuals with fewer than 30 quarters, the full Part A premium in 2025 is $518 per month.

- Failure to enroll in premium Part A when first eligible can result in a late enrollment penalty, increasing the premium by 10%. This penalty must be paid for twice the number of years the individual delayed enrollment.

Medicare Part B (Medical Insurance) Eligibility

Eligibility for Part B is linked to Part A eligibility.

- Anyone eligible for premium-free Part A is also eligible to enroll in Part B by paying the standard monthly premium (subject to income adjustments).

- Individuals who must pay a premium for Part A, or those who only want Part B coverage, must meet the following criteria: be age 65 or older, be a U.S. resident, AND be either a U.S. citizen or a lawfully admitted permanent resident who has lived in the U.S. for at least 5 continuous years.

Enrollment in Part B is optional. However, because it covers a wide range of essential outpatient medical services, it is a critical component of comprehensive health coverage for seniors. The decision to enroll requires careful consideration, particularly regarding existing health coverage and potential penalties for delaying enrollment without a valid reason.

3. Enrolling in Medicare: Process and Timing

The process for enrolling in Medicare varies depending on whether an individual is already receiving Social Security or Railroad Retirement Board (RRB) benefits.

Automatic Enrollment

Individuals who are already receiving retirement or disability benefits from Social Security or the RRB at least four months before turning 65 are typically enrolled in Medicare Part A and Part B automatically. Similarly, those under 65 who become eligible for Medicare due to disability will be automatically enrolled after receiving SSDI or RRB disability benefits for 24 months.

In these cases, a “Welcome to Medicare” package, including the Medicare card, is mailed out approximately three months before coverage is set to begin. No application is necessary for these individuals, although they will have the option to decline Part B coverage if desired (though penalties may apply if declined and later enrolled without creditable coverage). An exception exists for residents of Puerto Rico and those living in foreign countries, who are automatically enrolled in Part A but must actively elect Part B coverage.

Manual Application Process

Individuals who are approaching age 65 but are not yet receiving Social Security or RRB benefits must actively apply for Medicare.

- When to Apply: The ideal time to apply is during the Initial Enrollment Period (IEP). Applying in the three months before the 65th birthday month ensures coverage starts promptly on the first day of the birthday month.

- Where to Apply: Applications for Original Medicare (Part A and Part B) are processed by the Social Security Administration (SSA).

- How to Apply: There are three primary methods:

-

- Online: This is promoted by SSA as the easiest and fastest method. The process involves visiting SSA.gov/benefits/medicare, selecting the appropriate application (“Apply for Medicare Only” or the combined retirement/Medicare application), and logging into or creating a secure my Social Security account. The application typically takes 10-30 minutes. Applicants receive an on-screen receipt and an application number to track status.SSA provides an online checklist to help applicants prepare.

- Phone: Applicants can call SSA’s national toll-free number at 1-800-772-1213 (TTY 1-800-325-0778). Representatives are typically available 8 a.m. to 7 p.m. weekdays in most time zones, with multilingual support. Individuals with railroad employment history should call the RRB at 1-877-772-5772.

- In-Person: Applicants can visit their local Social Security office.SSA generally recommends calling ahead to make an appointment.

Information and Documents Needed for Application

Gathering necessary information and documents beforehand streamlines the application process. While SSA may already have some information on file or can assist in obtaining missing documents, being prepared is advisable.

- Information Required: Applicants should be prepared to provide:

-

- Personal Details: Full name, Social Security number (SSN), date and place of birth, gender, citizenship status.

- Spouse Information: Current/former spouse’s name, SSN, date of birth, dates/places of marriage, dates of divorce/death.

- Children Information: Names/ages of unmarried children under 18 (or 18-19 in school) or disabled before age 22.

- Financial Information: Bank routing and account numbers (for direct deposit of any potential benefits), earnings information for the last year, current year, and possibly an estimate for the next year.

- Health Insurance: Start and end dates for any current or past employer group health plans since age 65.

- Other: History of previous Social Security/Medicare/SSI applications, other SSNs used, military service dates (especially before 1968), recent inability to work due to illness/injury, railroad industry work history, foreign social security credits, federal/state/local government pension information.

- Documents Potentially Needed: SSA may request original documents (unless otherwise noted):

-

- Proof of Age: Original birth certificate (or a copy certified by the issuing agency). Other documents like immunization records or school records may be acceptable if a birth certificate is unavailable.

- Proof of Citizenship/Legal Residency: U.S. Passport, Certificate of Naturalization (N-550/N-570), Certificate of Citizenship (N-560/N-561), Consular Report of Birth Abroad (FS-240), or Permanent Resident Card (Green Card I-551). Required only if citizenship/status isn’t already established with SSA.

- Military Service: U.S. military service papers (e.g., DD-214) if service occurred before 1968.

- Work History: Copy of W-2 forms and/or self-employment tax return for the previous year.

- Important Note: SSA often requires original documents (like birth certificates or citizenship papers) but accepts photocopies of W-2s, tax returns, and medical documents. Originals are returned after review.If SSA already has proof of age or citizenship from a prior claim, resubmission may not be needed.Foreign birth records or DHS documents should ideally be presented in person at an SSA office.

- Specific Forms for Part B Special Enrollment Period (SEP): Individuals enrolling in Part B during an SEP after initially delaying due to employer coverage need to submit:

-

- Form CMS-40B: Application for Enrollment in Medicare Part B.

- Form CMS-L564: Request for Employment Information (completed by the employer if possible).

- Proof of Group Health Plan (GHP) or Large Group Health Plan (LGHP) coverage based on current employment (e.g., pay stubs showing premium deductions, W-2s with pre-tax contributions, health insurance cards, explanation of benefits).

4. Critical Medicare Enrollment Windows

Understanding the specific timeframes for enrollment is essential to avoid penalties and ensure timely coverage.

Initial Enrollment Period (IEP)

- Definition: The IEP is the primary window for individuals to enroll in Medicare when they first become eligible, typically around age 65.It is a 7-month period that includes:

-

- The 3 months before the month the individual turns 65.

- The month the individual turns 65.

- The 3 months after the month the individual turns 65.

- Example: If an individual’s 65th birthday is in July, their IEP runs from April 1st to October 31st.

- Special Case: If an individual’s birthday falls on the first day of the month, their IEP starts and ends one month earlier. For example, a June 1st birthday results in an IEP from February 1st to August 31st.

- Coverage Start Dates within IEP: The date Medicare coverage begins depends on when within the IEP the individual enrolls:

-

- Enrollment in the 1-3 months before the 65th birthday month: Coverage starts on the first day of the birthday month.This timing is crucial for avoiding any gap in coverage upon turning 65.

- Enrollment during the 65th birthday month or in the 1-3 months after: Coverage starts on the first day of the month following the enrollment month.

- Part A Retroactivity: For premium-free Part A, if an application is filed more than 6 months after turning 65, coverage can be retroactive for up to 6 months, but no earlier than the first month of eligibility.This retroactivity does not typically apply to Part B or premium Part A.

- Significance: Enrolling during the IEP is the standard way to get Medicare Part A and/or Part B without facing late enrollment penalties.It is highly recommended to enroll during the three months prior to the 65th birthday month to ensure coverage begins seamlessly.

Special Enrollment Period (SEP) for Employer Coverage

- Eligibility: This SEP is available for individuals who delay enrolling in Medicare Part B (and sometimes premium Part A) at age 65 because they have health coverage through a Group Health Plan (GHP) based on current employment – either their own or their spouse’s.It is critical that the coverage is based on current work; retiree health plans, COBRA continuation coverage, VA coverage, or individual health insurance (like Marketplace plans) generally do not qualify an individual to delay Medicare enrollment without penalty and use this SEP.Individuals should confirm with their employer or benefits administrator if their plan qualifies, especially if the employer has fewer than 20 employees, as Medicare might be the primary payer regardless.

- Timing: The SEP allows enrollment in Part B:

-

- At any time while the individual (or their spouse) is still working AND covered by the GHP.

- During the 8-month period that begins the month after the employment ends OR the GHP coverage based on that employment ends, whichever occurs first.

- Coverage Start Dates within SEP:

-

- If enrolling while still employed/covered or in the first month of the 8-month window: Coverage can begin the first day of the month of enrollment, or the individual can choose to delay the start date up to three months.

- If enrolling during months 2 through 8 of the 8-month window: Coverage begins the first day of the month after enrollment.

- Significance: The SEP provides flexibility for working individuals (and their covered spouses) to maintain employer coverage past age 65 and enroll in Part B later without incurring a late enrollment penalty.

General Enrollment Period (GEP)

- Timing: If an individual misses their IEP and does not qualify for an SEP, the next opportunity to enroll in Part B (and premium Part A) is during the GEP, which runs from January 1st to March 31st each year.

- Coverage Start Date: For enrollments during the GEP, coverage begins on the first day of the month after enrollment. This is a change from previous rules where coverage began July 1st.

- Penalties: Enrolling during the GEP almost always means the individual will face a late enrollment penalty for Part B (and potentially premium Part A).This penalty is typically lifelong for Part B.

- Significance: The GEP serves as a fallback enrollment window but should generally be avoided due to the associated penalties and potential for coverage delays compared to the IEP or SEP.

Summary of Enrollment Periods

Enrollment Period Who It’s For Timeframe Coverage Start Date Penalty Risk Initial Enrollment Period (IEP)Individuals first becoming eligible for Medicare (usually turning 65)7 months (3 months before, month of, 3 months after 65th birthday)Month of 65th birthday (if enroll before); Month after enrollment (if enroll during/after birthday month)No penalty if enrolled during IEPSpecial Enrollment Period (SEP)Individuals delaying Part B due to current employer GHP coverage (self/spouse)1. Anytime while working/covered

2. 8 months after employment/coverage ends Month of enrollment or up to 3 months later (if enroll while covered/1st month after); Month after enrollment (if enroll months 2-8)No penalty if eligible for SEP General Enrollment Period (GEP)Individuals who missed IEP and don’t qualify for SEPJanuary 1 – March 31 each year Month after enrollment Likely penalty applies

5. Medicare Part B (Medical Insurance): Coverage, Costs, and Considerations

Medicare Part B provides coverage for a wide array of outpatient medical services and supplies necessary for diagnosing and treating medical conditions, as well as preventive care.

Covered Services

Part B helps cover:

- Medically Necessary Services: Services from doctors and other healthcare providers, outpatient hospital services, clinical laboratory services, diagnostic tests (like X-rays, MRIs), and some surgeries performed on an outpatient basis.

- Preventive Services: Healthcare aimed at preventing illness or detecting it early, such as flu shots, mammograms, colonoscopies, cardiovascular screenings, diabetes screenings, and the annual “Wellness” visit. Many preventive services are covered at $0 cost-sharing if received from a provider who accepts Medicare assignment.

- Durable Medical Equipment (DME): Items like wheelchairs, walkers, hospital beds, oxygen equipment, and blood sugar monitors needed for use in the home.

- Other Services: Ambulance services, mental health services (inpatient, outpatient, partial hospitalization), limited outpatient prescription drugs (often those administered in a clinical setting, like some chemotherapy drugs or drugs used with DME), physical therapy, occupational therapy, and some home health care.

- Insulin for Pumps: For beneficiaries using an insulin pump covered under the DME benefit, the monthly cost for Part B-covered insulin cannot exceed $35, and the Part B deductible does not apply to this benefit.

Part B Costs in 2025

Enrolling in Part B involves several cost components:

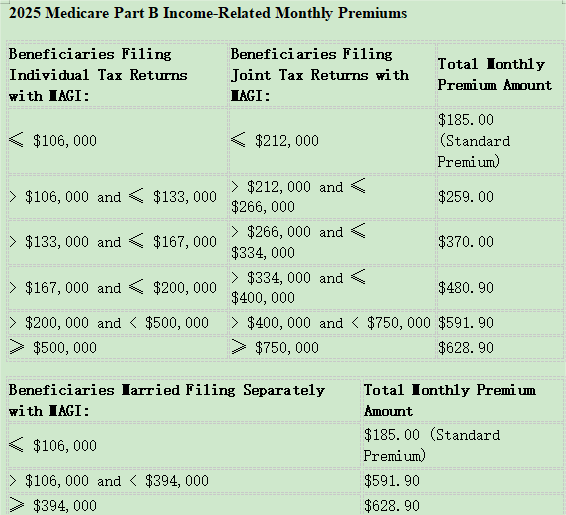

- Monthly Premium: Most beneficiaries pay the standard monthly premium, which is $185.00 for 2025.This premium is paid monthly, regardless of whether Part B services are used.

- Annual Deductible: Before Medicare begins paying its share for most Part B services, beneficiaries must meet an annual deductible. For 2025, the Part B deductible is $257.

- Coinsurance: After the deductible is met, beneficiaries typically pay 20% of the Medicare-approved amount for most doctor services, outpatient therapy, and DME. Medicare pays the remaining 80%.

- Income-Related Monthly Adjustment Amount (IRMAA): Beneficiaries with higher incomes pay an additional amount added to their standard monthly premium. This adjustment is based on the Modified Adjusted Gross Income (MAGI) reported on IRS tax returns from two years prior. Approximately 8% of beneficiaries pay IRMAA.

The following table details the 2025 total monthly Part B premiums, including IRMAA, based on 2023 MAGI:

(Source: CMS.gov Fact Sheet, Nov 2024)

(Source: CMS.gov Fact Sheet, Nov 2024)

The Value and Necessity of Part B

Medicare Part B provides essential coverage for a wide range of outpatient medical needs, including doctor visits, diagnostic tests, preventive screenings, and medical equipment.Its value extends beyond treating illness; the inclusion of numerous preventive services, often at no cost-sharing, promotes early detection and health maintenance.

For most beneficiaries, Part B is highly cost-effective due to significant government subsidies covering approximately 75% of the program’s costs.Without Part B or equivalent creditable coverage (like that from a current employer), individuals would be responsible for the full cost of these medical services, potentially facing substantial medical bills, especially if unexpected health issues arise.Therefore, Part B is generally considered a necessary component of health coverage for individuals turning 65 unless they qualify to delay enrollment.

Deciding Whether to Enroll in Part B at 65

The primary factor in deciding whether to enroll in Part B during the IEP is the presence of other health coverage. If an individual (or their spouse) has GHP coverage based on current employment, they may be eligible to delay Part B enrollment without penalty and use the SEP later.It is crucial to verify that the coverage meets the specific requirements for the SEP, as retiree, COBRA, or individual plans typically do not qualify.Consulting with the employer’s benefits administrator is recommended.

Consequences of Delaying Part B Enrollment (Without Creditable Coverage)

Delaying Part B enrollment beyond the IEP without having qualifying GHP coverage based on current employment leads to significant negative consequences:

- Late Enrollment Penalty: A penalty is added to the monthly Part B premium. This penalty is calculated as 10% of the standard premium for each full 12-month period the individual was eligible for Part B but did not enroll.Critically, this penalty is permanent and must be paid for as long as the individual has Part B coverage.

-

- Example: Delaying enrollment for 2 full years results in a 20% penalty. Based on the 2025 standard premium of $185.00, the penalty would be $37.00 ($185.00 x 0.20), making the total monthly premium $222.00 (rounded to the nearest $0.10).

- Coverage Gaps: Individuals who delay enrollment and do not qualify for an SEP must wait for the GEP (January 1 – March 31) to sign up.Coverage will not begin until the month after enrollment.This delay creates a gap in coverage, potentially lasting several months, during which the individual is uninsured for Part B services and fully liable for the costs of any outpatient medical care received.

These dual consequences – a permanent financial penalty and the risk of being uninsured and facing high medical bills during a coverage gap – underscore the importance of timely Part B enrollment unless one definitively qualifies for an SEP based on active employer coverage.

6. Medicare Part D (Prescription Drug Coverage): Coverage, Costs, and Considerations

Medicare Part D provides optional coverage for outpatient prescription drugs, helping beneficiaries manage medication costs.

Covered Services

Part D plans help pay for brand-name and generic prescription drugs.These are typically medications beneficiaries pick up at a pharmacy or receive through mail order, rather than drugs administered in a hospital or clinic setting (which may be covered under Part A or Part B).Part D also covers many commercially available vaccines not covered by Part B, insulin and related supplies (like syringes), and smoking cessation drugs.

How Part D Plans Work

Part D coverage is delivered exclusively through private insurance companies that contract with Medicare.Beneficiaries can obtain Part D coverage through:

- Standalone Prescription Drug Plans (PDPs): These plans add drug coverage to Original Medicare (Parts A and B) or certain other Medicare plans like Cost Plans or some Private Fee-for-Service (PFFS) plans.

- Medicare Advantage Prescription Drug Plans (MA-PDs): These plans bundle Parts A, B, and D coverage together.

Key features of how these private plans operate include:

- Formularies: Each plan has its own list of covered drugs, called a formulary.While plans must cover at least two drugs in the most commonly prescribed categories and virtually all drugs in certain “protected classes” (like medications for cancer, HIV/AIDS, depression, etc.), the specific drugs covered vary significantly from plan to plan.Formularies are subject to change annually.

- Tiers: Plans typically group drugs into different tiers on their formulary, each with a different cost-sharing level.Generally:

-

- Tier 1: Lowest copayment (often preferred generics)

- Tier 2: Medium copayment (often other generics or preferred brands)

- Tier 3: Higher copayment (often non-preferred brands)

- Specialty Tier: Highest cost-sharing (very expensive drugs)

- A drug in a lower tier costs less out-of-pocket than a drug in a higher tier.Beneficiaries can request an exception from their plan for lower cost-sharing on a higher-tier drug if their prescriber deems it medically necessary.

- Pharmacy Networks: Plans contract with a network of pharmacies.Using pharmacies within the plan’s network, especially “preferred” pharmacies, usually results in lower out-of-pocket costs compared to using out-of-network pharmacies.Mail-order pharmacy options may also offer savings.

Because of this variability, it is essential for beneficiaries to compare Part D plans each year during the Medicare Open Enrollment period (October 15 – December 7) based on their specific medication needs, preferred pharmacies, and overall costs.Tools like the Medicare Plan Finder on Medicare.gov facilitate this comparison.

Part D Costs and Coverage Stages in 2025

Part D costs include premiums, deductibles, and cost-sharing (copayments/coinsurance). A significant change takes effect in 2025 with the implementation of a $2,000 annual cap on out-of-pocket drug spending.

- Premium: Monthly premiums vary widely by plan.

-

- The 2025 estimated average monthly premium for standalone PDPs is $45.

- The 2025 estimated average monthly premium for drug coverage within MA-PDs is $7.

- The 2025 national base beneficiary premium (used for penalty calculations) is $36.78.

- Higher-income beneficiaries pay an IRMAA in addition to their plan premium.

- Deductible: The amount paid before the plan starts sharing costs. This varies by plan but cannot exceed $590 in 2025.Some plans have a $0 deductible.

- Cost-Sharing (Copayments/Coinsurance): The amount paid per prescription after the deductible (if any) is met. This varies by drug tier and plan.

- 2025 Coverage Stages: The structure simplifies significantly in 2025:

-

- Deductible Stage: The beneficiary pays 100% of drug costs until the plan’s deductible (up to $590) is met.

- Initial Coverage Stage: After the deductible, the beneficiary generally pays 25% coinsurance for covered drugs.This continues until the beneficiary’s total out-of-pocket (OOP) spending reaches $2,000.This OOP amount includes the deductible paid and the 25% coinsurance paid during this stage.

- Catastrophic Coverage Stage: Once the beneficiary’s OOP spending reaches the $2,000 cap, they enter the catastrophic stage and pay $0 (zero dollars) for all covered prescription drugs for the remainder of the calendar year.This effectively eliminates the previous “coverage gap” or “donut hole.”

Visualizing the 2025 Part D Stages:

Imagine a progress bar representing annual out-of-pocket drug costs:

- Start (Year Begins): Beneficiary pays 100% of costs.

- Deductible Met (up to $590): Beneficiary now pays 25% coinsurance.

- $2,000 Out-of-Pocket Reached: Beneficiary pays $0 for covered drugs for the rest of the year.

The Value and Necessity of Part D

Part D coverage provides essential financial protection against the often high and unpredictable costs of prescription medications. The introduction of the $2,000 annual out-of-pocket cap in 2025 dramatically increases the value of Part D. It transforms the benefit from simply reducing drug costs to providing a hard ceiling on annual drug expenditures, offering significant peace of mind and financial security, particularly for those with high drug needs.

Even for individuals who currently take few or no medications, enrolling in a low-premium Part D plan during the IEP is generally advisable. This strategy avoids the permanent late enrollment penalty that would apply if coverage is needed later. Furthermore, the Extra Help program provides substantial assistance with premiums, deductibles, and copayments for beneficiaries with limited income and resources, making coverage highly affordable for those who qualify. Given the potential for high drug costs and the permanent nature of the penalty, Part D is a valuable, and often necessary, component of Medicare coverage for nearly all beneficiaries.

Deciding Whether to Enroll in Part D at 65

Similar to Part B, the decision to delay Part D hinges on having other creditable prescription drug coverage. Creditable coverage is drug coverage (e.g., from an employer, union, VA, TRICARE) that is expected to pay, on average, at least as much as standard Medicare Part D. Individuals with such coverage can delay Part D enrollment without penalty. However, they must enroll in a Medicare Part D plan within 63 days of losing that creditable coverage to avoid the penalty. Health plans providing drug coverage are required to notify their members annually whether the coverage is creditable. It is crucial for individuals relying on non-Medicare coverage to confirm its creditable status and keep documentation.

Consequences of Delaying Part D Enrollment (Without Creditable Coverage)

Delaying enrollment in a Medicare Part D plan beyond the IEP without having other creditable drug coverage results in:

- Late Enrollment Penalty: This penalty is calculated as 1% of the national base beneficiary premium ($36.78 in 2025) for each full month the individual went without creditable coverage after their IEP ended. This amount is rounded to the nearest $0.10 and added to the individual’s monthly Part D premium. Like the Part B penalty, this penalty is permanent and is paid for as long as the individual has Part D coverage. Because the penalty accrues monthly, it can increase rapidly compared to the Part B penalty.

-

- Example: Delaying Part D enrollment for 14 months without creditable coverage results in a 14% penalty. In 2025, this would be $5.20 per month (1% x $36.78 x 14 months = $51.49/year, or $5.15 per month, rounded to $5.20) added to the chosen plan’s premium.

- Exposure to High Drug Costs: Without Part D or other creditable coverage, individuals are responsible for 100% of their prescription drug costs. This lack of coverage can lead to significant financial strain, potentially forcing difficult choices between necessary medications and other essential expenses, especially if high-cost specialty drugs are required.

7. Making Informed Decisions About Part B and Part D

Navigating Medicare enrollment requires careful consideration of individual circumstances. Key factors influencing the decision to enroll in Part B and Part D during the Initial Enrollment Period include:

- Current and Future Health Needs: Assessing current health status and anticipating the potential need for doctor visits, medical treatments, or prescription drugs.

- Existing Coverage: Determining if current health insurance (especially employer-sponsored) qualifies as “creditable coverage” allowing for penalty-free delay of Part B and/or Part D. Verification with the plan provider is essential.

- Costs: Understanding the 2025 premiums, deductibles, and cost-sharing structures for both Part B and Part D, including potential IRMAA adjustments based on income.

- Risks of Delay: Recognizing the significant and often permanent financial penalties associated with late enrollment, as well as the potential for costly coverage gaps if enrollment is delayed without qualifying creditable coverage.

- Enrollment Windows: Knowing the dates of the personal Initial Enrollment Period and understanding the rules for Special Enrollment Periods and the General Enrollment Period.

Individuals approaching 65 should engage in proactive planning well before their IEP begins. This includes verifying eligibility for premium-free Part A, confirming the status of any existing health coverage, gathering necessary documents, and utilizing official resources like Medicare.gov and SSA.gov. State Health Insurance Assistance Programs (SHIPs) can also offer free, unbiased counseling.

8. Conclusion and Next Steps

Enrolling in Medicare is a critical step for securing healthcare coverage upon reaching age 65. Understanding eligibility rules, the distinct functions of Medicare Parts A, B, and D, and the specific enrollment periods (IEP, SEP, GEP) is essential for making timely and informed decisions.

Medicare Part B provides vital coverage for doctor visits, outpatient services, and preventive care, while Medicare Part D offers crucial protection against high prescription drug costs, enhanced significantly by the $2,000 out-of-pocket cap starting in 2025. Delaying enrollment in either Part B or Part D without having qualifying creditable coverage based on current employment can lead to permanent monthly premium penalties and potentially dangerous gaps in coverage, exposing individuals to significant financial risk.

Individuals nearing age 65 are strongly encouraged to:

- Verify Eligibility: Confirm eligibility for premium-free Part A and understand Part B requirements.

- Assess Current Coverage: Determine if existing employer health or drug coverage is “creditable” and allows for penalty-free delay.

- Gather Information: Collect necessary personal information and documents required for the application.

- Enroll Timely: Apply for Medicare Parts A and B through the Social Security Administration during the Initial Enrollment Period, ideally 1-3 months before the 65th birthday month to ensure coverage starts on time.

- Consider Part D: Enroll in a Medicare Part D plan during the IEP to secure drug coverage and avoid the permanent late enrollment penalty, unless maintaining verified creditable drug coverage.

- Utilize Resources: Consult official websites and helplines for accurate information and assistance.

Key Resources:

- Medicare Official Website: Medicare.gov

- Medicare Phone: 1-800-MEDICARE (1-800-633-4227) (TTY: 1-877-486-2048)

- Social Security Administration Website: SSA.gov

- Social Security Phone: 1-800-772-1213(TTY: 1-800-325-0778)

- Railroad Retirement Board (if applicable): RRB.gov or 1-877-772-5772

By taking proactive steps and understanding the enrollment process and coverage options, individuals can successfully navigate their transition into Medicare and secure the health coverage they need